In this Helcim review, I break down its pricing model, payment features, hardware options, and where it outperforms competing processors. Learn whether Helcim is the right fit for small and midsize businesses focused on lowering long-term payment processing costs.

Helcim fast facts

- My rating: 4.58 out of 5

- Pricing: $0 per month

- Key features:

- Interchange-plus pricing with automatic volume discounts

- All-in-one merchant account

- Invoicing and recurring billing

- Helcim Fee Saver

- Helcim Card Reader

- Payment Extension for embedded payments

Helcim is a payment processor and merchant account provider built for small and midsize businesses that want transparent pricing and fewer add-on fees. Unlike many competitors, Helcim uses interchange-plus pricing with automatic rate reductions as processing volume increases, making it especially attractive for growing businesses with predictable card volume.

In our evaluation, Helcim earned top marks for pricing transparency, account stability, and core payment functionality; it ranks as our top payment processor overall. It offers built-in tools for invoicing, recurring billing, and chargeback management without long-term contracts, making it a strong choice for businesses that prioritize lower processing costs over expansive software ecosystems.

Helcim’s use cases

I recommend Helcim for:

- Growing small and midsize businesses: Interchange-plus pricing with automatic volume discounts helps reduce processing costs as transaction volume increases.

- Businesses that want pricing transparency: Helcim avoids flat-rate markups, long-term contracts, and early termination fees, making costs easier to predict.

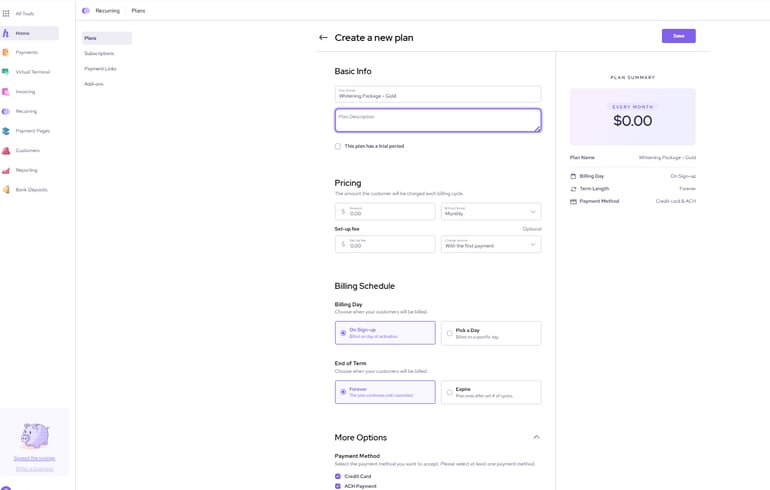

- Merchants that invoice or bill recurring customers: Built-in invoicing, recurring billing, and subscription tools are included at no extra cost.

- Omnichannel sellers: Helcim supports in-person, online, keyed, and mobile wallet payments through a single merchant account.

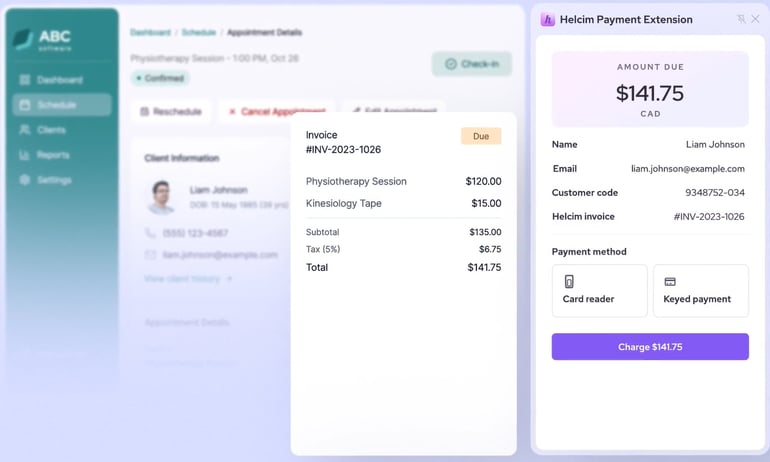

- Software-driven or vertical businesses: The Helcim Payment Extension allows payments to run directly inside existing ERMs, appointment systems, and management software without workflow changes.

- Cost-focused operators: Helcim is a strong fit for businesses that prioritize lower effective processing rates over large app ecosystems or bundled commerce tools.

Helcim’s pricing

- Monthly account fee: $0

- Virtual terminal fee: $0/month

- American Express transactions: + 0.10% + $0.10

- ACH fee: 0.5% + $0.25 per transaction

- Invoice fee: $0

- Chargeback fee: $15 refundable

- Payment processing fees:

| Monthly volume | In-person rate | Keyed & online rate |

|---|---|---|

| $0 - $50K | Interchange+ 0.40% + 8 cents | Interchange+ 0.50% + 25 cents |

| $50K - $100K | Interchange+ 0.35% + 7 cents | Interchange+ 0.45% + 20 cents |

| $100K - $500K | Interchange+ 0.25% + 7 cents | Interchange+ 0.35% + 20 cents |

| $500K - $1M | Interchange+ 0.20% + 6 cents | Interchange+ 0.25% + 15 cents |

| $1M+ | Interchange+ 0.15% + 6 cents | Interchange+ 0.15% + 15 cents |

Helcim’s hardware

Helcim offers flexible in-person payment options for small and midsize businesses, including dedicated hardware and mobile-based acceptance. In addition to its physical terminals, Helcim supports Tap to Pay on iPhone, allowing merchants to accept contactless payments directly on an iPhone without additional hardware, which is useful for mobile sellers, service businesses, and pop-up locations.

Helcim Card Reader

- Payment types: Tap, insert, and PIN; supports Apple Pay and Google Pay

- Display: 4-inch color LCD with capacitive multi-touch

- Operating system: Secure Android 13

- Performance: A53 quad-core 2.0GHz processor, 2GB RAM, 8GB flash storage

- Connectivity: Wi-Fi and 4G LTE

- Portability: Lightweight, handheld design (160g)

- Notable features: In-person surcharging via Helcim Fee Saver; standalone processing mode planned

- Price: $199

Helcim Smart Terminal

- Payment types: EMV chip cards, contactless payments, and mobile wallets

- Display: 6.7-inch HD+ touchscreen for faster, more intuitive checkout

- Operating system: Android 13

- Performance: Octa-core 2.4GHz processor for smooth, responsive operation

- Connectivity: Built-in 4G LTE and Wi-Fi for mobile and fixed-location use

- Battery: 3350mAh, 7.4V battery with up to 12 hours of operation per charge

- Built-in printer: Integrated thermal printer with 100mm/sec print speed

- Portability: Compact and lightweight design (192 × 81 × 54 mm; 436g)

- Security: PCI-compliant with secure tokenization for returning customers

- Best suited for: Retail, hospitality, and service businesses that need a portable all-in-one terminal with receipt printing

- Price: $349 or $32 per month for 12 months

Helcim’s key features

Helcim focuses on core payment functionality that helps small and midsize businesses reduce processing costs, simplify billing, and manage payments across channels without relying on third-party add-ons. Here are some of the standout features of Helcim that I liked the most:

Interchange-plus pricing with volume discounts

Helcim uses interchange-plus pricing and automatically reduces its markup as monthly processing volume increases. This transparent pricing model can result in lower effective rates over time compared to flat-rate processors, especially for growing businesses with predictable transaction volume.

All-in-one merchant account

Helcim provides a dedicated merchant account rather than operating as a payment aggregator. This improves account stability and reduces the risk of sudden fund holds, making it a better fit for businesses with consistent transaction volume.

Invoicing and recurring billing

Helcim includes built-in tools for one-time invoices, recurring billing, and subscription management at no additional cost. Businesses can accept card and ACH payments directly from invoices, helping streamline billing and cash flow.

Omnichannel payment acceptance

Merchants can accept payments in person, online, via invoice, keyed entry, and mobile wallets under a single Helcim account. Reporting and transaction data are centralized, making it easier to reconcile payments across channels.

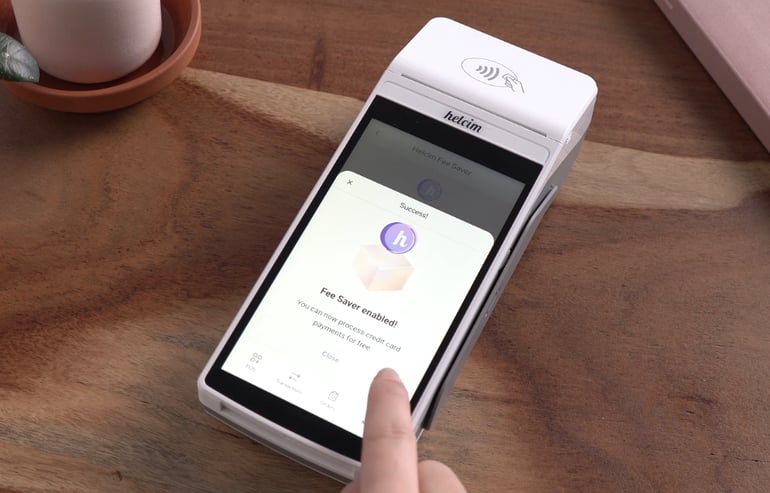

Helcim Fee Saver

Helcim Fee Saver allows eligible merchants to pass credit card processing fees on to customers for in-person transactions, where permitted by law. This feature can significantly reduce out-of-pocket processing costs for businesses operating on tight margins.

Integration Marketplace

Helcim’s Integration Marketplace offers connections to a solid mix of popular ecommerce platforms, accounting tools, and business software. While its integration catalog isn’t as extensive as those of larger ecosystems like PayPal or Shopify, it covers many commonly used platforms and is supplemented by the Helcim Payment Extension for more specialized workflows.

Helcim Payment Extension

The Helcim Payment Extension allows businesses to embed secure payment processing directly into existing software, such as ERMs, appointment systems, and shop management platforms. This enables in-person and keyed payments without changing workflows or retraining staff.

Helcim’s pros and cons

| Pros | Cons |

|---|---|

| ✅ Transparent interchange-plus pricing with automatic volume discounts | ❌ Limited hardware options for larger or more complex POS environments |

| ✅ No long-term contracts or early termination fees | ❌ Not tailored to specific industries like restaurants or retail franchises |

| ✅ Dedicated merchant accounts with strong account stability | ❌ Limited bundled business and commerce software |

| ✅ Built-in invoicing and recurring billing tools | |

| ✅ Multiple in-person payment options, including Tap to Pay on iPhone |

Alternatives to Helcim

While Helcim is a strong choice for businesses that prioritize transparent pricing and lower long-term processing costs, it may not be the best fit for every use case. Businesses that need industry-specific tools, larger POS hardware ecosystems, or bundled commerce features may benefit from exploring alternative payment platforms.

| Best for | | |||

| Monthly price | ||||

| Transaction fees | ||||

| Industry-specific POS tools | ||||

| Large hardware ecosystem | ||||

Square

Square is a better fit for retail and restaurant businesses that need industry-specific POS features, inventory tools, and a broad range of hardware options. Its flat-rate pricing is simpler but can be more expensive than Helcim at higher volumes.

Stripe

Stripe is ideal for online-first and software-driven businesses that need powerful APIs, custom checkout flows, and global payment support. However, it lacks in-person hardware depth and uses flat-rate pricing that can be less cost-effective over time.

PayPal

PayPal works well for businesses that want fast setup and access to a large consumer payment network. While flexible, its pricing structure and account stability may be less appealing for businesses processing higher volumes or seeking a traditional merchant account.

My methodology

I evaluated Helcim using the same scoring framework applied in TechRepublic’s roundup of the best payment processing companies. The review assesses pricing transparency, payment features, ease of use, account stability, hardware options, integrations, and overall value for small and midsize businesses.

Scores are based on a combination of hands-on product research, publicly available pricing and documentation, feature comparisons against competing platforms, and how well Helcim serves common SMB payment use cases. The final rating reflects Helcim’s strengths in transparent pricing and core payment functionality, balanced against limitations in hardware depth and industry-specific tools.

Frequently asked questions (FAQs)

Is Helcim a payment processor or a merchant account provider?

Helcim is both. It provides payment processing services and a dedicated merchant account, rather than operating as a third-party payment aggregator.

Does Helcim charge monthly fees or long-term contracts?

No. Helcim does not charge monthly subscription fees, require long-term contracts, or impose early termination fees.

What payment methods does Helcim support?

Helcim supports in-person, online, invoiced, keyed, and recurring payments, as well as mobile wallets like Apple Pay and Google Pay. It also supports Tap to Pay on iPhone for contactless payments without additional hardware.

Can Helcim integrate with my existing software?

Yes. Helcim offers native integrations with popular ecommerce and accounting platforms, and its Payment Extension allows payments to be embedded directly into many industry-specific systems.

Is Helcim suitable for restaurants or retail POS systems?

Helcim supports in-person payments but does not offer industry-specific POS software. Restaurants or multi-location retail businesses may prefer platforms with specialized POS tools.

Does Helcim support surcharging?

Yes. Helcim’s Fee Saver feature allows eligible merchants to pass credit card processing fees to customers for in-person transactions, where permitted by law.