A business bank statement is an official financial document issued by a bank that records all transactions made within a specific timeframe. It provides a comprehensive view of your business’s financial activity — including deposits, withdrawals, bank fees, and checks cleared.

In this guide, I’ll go over a business bank statement’s key components, provide a business bank statement example, and discuss the benefits of tracking your statements effectively.

- Business bank statement example

- Key components of a business bank statement

- Understanding fees and charges on a business bank statement

- Business bank statements and tax preparation

- Benefits of monitoring a business bank statement

- How to reconcile a business bank statement

- What to do if there’s an error in a business bank statement

- Automated tools for tracking business bank statements

- Personal vs business bank statement

- Frequently asked questions (FAQs)

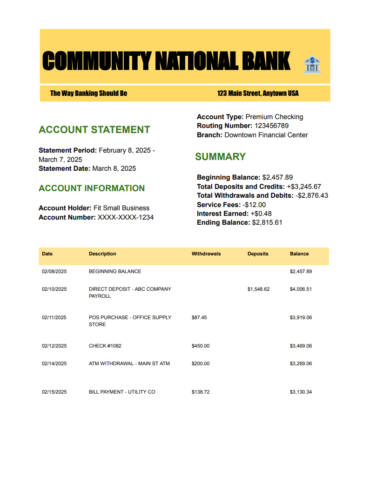

Business bank statement example

By analyzing a business bank statement sample, you can gain insights into your business’s financial health, identify discrepancies, and make informed decisions about operations. Over the years, I’ve helped many businesses with questions about their bank statements.

Below is an example of a business bank statement to illustrate how financial data is organized.

Key components of a business bank statement

With so many different sections on a bank statement, understanding each is helpful. Below is a breakdown of the key parts.

1. Heading

- Statement period

- Statement date

- Business name

- Truncated account number

2. Summary of account activity

- Beginning balance: The balance at the start of the statement period

- Total deposits: The sum of all incoming funds

- Total withdrawals and debits: The sum of all outgoing transactions

- Service fee: Any additional fees charged during the statement period

- Interest earned: These are paid dividends

- Ending balance: The balance at the end of the period

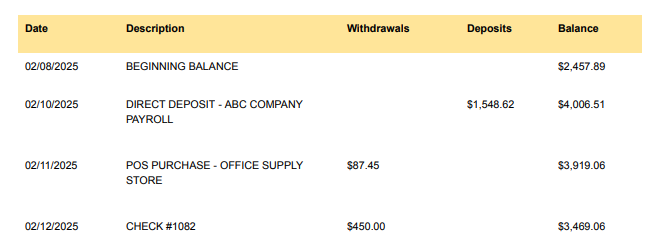

3. Transaction details

- Date: The date of each transaction

- Description: A brief summary of the transaction (e.g., vendor payment, customer deposit)

- Amount: The value of the transaction, either credited or debited

- Running balance: The account balance after each transaction

Understanding fees and charges on a business bank statement

Business bank statements often include various fees that can add up over time, such as monthly maintenance, overdraft, wire transfer, and transaction fees. Understanding business bank account fees can help you find ways to reduce costs.

Some banks waive fees if you maintain a minimum balance, use online banking, or bundle services. If you notice unexpected charges on your statement, review your bank’s fee schedule and consider switching to an account with better terms. Keeping track of fees ensures that your banking costs remain manageable and don’t eat into your profits.

Business bank statements and tax preparation

Business bank statements play a vital role in tax preparation by providing a clear record of income, expenses, and deductions. Many tax deductions — such as office expenses, travel, and vendor payments — can be validated using bank statements.

When filing taxes, you should cross-reference statements with receipts and invoices to ensure accuracy. Keeping well-organized and categorized statements can streamline tax filing, reduce errors, and help avoid potential audits.

Benefits of monitoring a business bank statement

- Financial planning and budgeting

- ✔ Helps track income and expenses

- ✔ Allows for better forecasting and financial decision-making

- Fraud detection and error resolution

- ✔Identifies unauthorized transactions

- ✔Helps catch errors before they impact cash flow

- Tax preparation and compliance

- ✔Organizes records for tax filing

- ✔Ensures accuracy in reporting business income and expenses

- Loan and credit applications

- ✔Provides documentation required by lenders to assess financial stability

- ✔Demonstrates ability to repay loans

How to reconcile a business bank statement

Reconciling your business bank statement is a crucial process to ensure your financial records match your bank’s reported transactions.

- Step 1: Compare balances. Check that the opening balance in your records matches the bank statement, then investigate discrepancies.

- Step 2: Match transactions. Verify deposits, withdrawals, and expenses against your records, and look for missing or unauthorized transactions.

- Step 3: Adjust for fees and interest. Record any bank fees, charges, or interest earned that aren’t in your records.

- Step 4: Resolve discrepancies. Investigate errors, correct bookkeeping mistakes, and report unauthorized charges.

- Step 5: Finalize and save. Ensure the adjusted balance matches the bank statement, and then keep a record for tax and audit purposes.

How long should you keep business bank statements? The IRS recommends retaining bank statements for three to seven years, depending on the nature of the transactions. Doing so is essential for tax compliance, financial audits, historical record-keeping, and loan applications.

Digital storage is often preferable to paper records, as it reduces clutter and ensures secure, long-term accessibility. You can also use cloud accounting software or secure local backups to organize statements efficiently.

What to do if there’s an error in a business bank statement

If you notice discrepancies on your business bank statement, do the following:

- Step 1: Review the transaction details carefully.

- Step 2: Compare with your accounting records to ensure accuracy.

- Step 3: Contact your bank’s customer support for resolution.

- Step 4: Dispute unauthorized charges promptly to prevent financial losses.

Automated tools for tracking business bank statements

Managing business bank statements manually can be time-consuming, but automation tools can simplify the process.

- The best small business accounting software like QuickBooks, Xero, or Wave integrates with bank accounts to automatically import transactions, categorize expenses, and generate reports.

- The best bank reconciliation software has features that flag discrepancies, reducing errors and saving time. Automated tracking ensures real-time financial visibility, making it easier to monitor cash flow, prepare for taxes, and make data-driven decisions.

By leveraging technology, your business can improve financial efficiency and avoid costly mistakes.

Personal vs business bank statement

| Personal bank statement | Business bank statement |

|

|---|---|---|

| Account holder | Individual | Business entity |

| Record-keeping | Personal expenses, salary deposits | Business income, expenses, and payroll |

| Record-keeping | Simpler | More detailed for accounting and tax purposes |

| Loan requirements | Used for personal loans | Required for business financing |

Business bank statements are more detailed and crucial for financial reporting, while personal statements are typically used for individual expense tracking.

Frequently asked questions (FAQs)

How do I get a business bank statement from my bank?

Most banks allow you to download your business bank statement through online banking.

- Log in to your online banking account.

- Navigate to the “Statements” or “Documents” section.

- Select the statement period.

- Download the file in PDF, CSV, or XLS format.

You can also request paper copies by visiting a branch or calling customer service.

Why do lenders ask for business bank statements when applying for a loan?

Lenders use business bank statements to assess a company’s financial health, cash flow stability, and ability to repay debt. They review income, expenses, and average balances to determine creditworthiness before approving a loan.

What should I do if I notice an unauthorized transaction on my business bank statement?

If you spot an unauthorized transaction, contact your bank immediately to report the issue. Most banks have fraud protection policies and may help recover lost funds. Also, review past statements to check for other suspicious activity and consider updating account security measures.