I like to think of inventory accounting like managing your smartphone apps.

You keep track of what is installed (inventory levels), what is used most often (inventory movement), and what takes up the most space (value). You create value (sales) by clearing out space. To clear that space, you might employ the First-In-First-Out (FIFO) method and delete older, unused apps first. Or you could use the Last-In-First-Out (LIFO) method and leave the old apps and clear out newer ones.

Regardless of the chosen method, your end goal is the same — monitoring and managing the items you use to create value. Inventory accounting is the process of valuing and tracking a company’s inventory assets. It plays a vital role in determining cost of goods sold (COGS), managing operations efficiently, and generating accurate financial statements.

- Overview of inventory & inventory accounting

- Types of Inventory

- How inventory accounting affects financial statements

- Examples of inventory accounting methods

- Example of inventory accounting using FIFO

- Example of inventory accounting using LIFO

- Example of inventory accounting using the Weighted Average method

- Example of inventory accounting using the specific identification method

- Which inventory method is best?

- Best practices for inventory accounting

- Bottom line

- Frequently asked questions (FAQs)

Overview of inventory & inventory accounting

What is inventory?

Inventory is the collection of goods a business holds and expects to sell to customers. Since businesses use inventory to meet customer demand, managing inventory helps prevent overstocking or running out of items. Since inventory is expected to be sold within a year, it appears on the balance sheet under current assets.

What is inventory accounting?

Inventory accounting is the practice of recording, analyzing, and reporting a company’s inventory transactions and balances. This practice helps determine the cost of sales and the value of remaining inventory.

Here are the key elements of inventory accounting:

- Tracking: Monitoring inventory levels, movement, and usage.

- Valuation methods: Employing different accounting techniques such as FIFO, LIFO, and Weighted Average.

Inventory can be tracked using a perpetual system or a periodic system. The perpetual system updates inventory records in real time with each sale or purchase, providing continuous accuracy. The periodic inventory system updates records at set intervals, relying on physical counts to determine inventory levels and cost of goods sold.

If you’re having trouble tracking inventory, I recommend Square, as it is an all-in-one sales system.

Types of Inventory

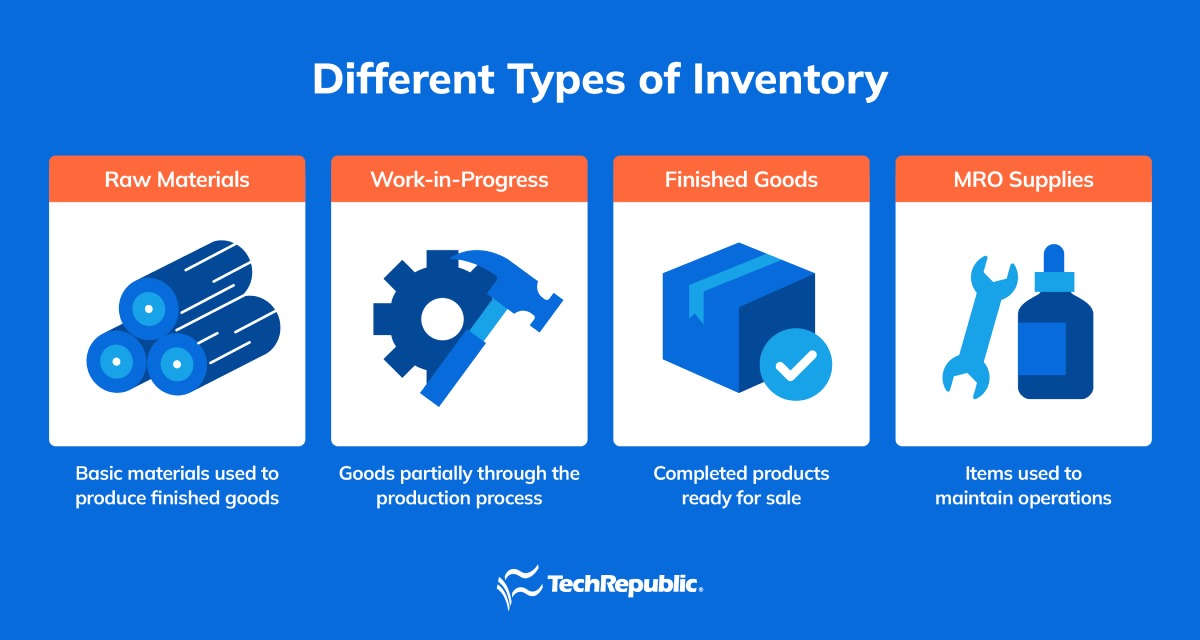

Inventory types are separated by stage of development, ranging from raw materials to finished goods. Here is a quick summary of inventory in its different stages of development.

| Raw Materials | Basic inputs used to produce goods |

| Work-In-Progress (WIP) | Semi-finished goods, still in production |

| Finished Goods | Completed products ready for sale |

| MRO Supplies | Items used to maintain operations (tools, lubricants, etc.) |

Maintenance, repair, and operations (MRO) supplies are materials used to keep a company’s operations running smoothly. These items are not directly part of the finished product. Instead, they are tracked separately from production inventory, due to their supporting role.

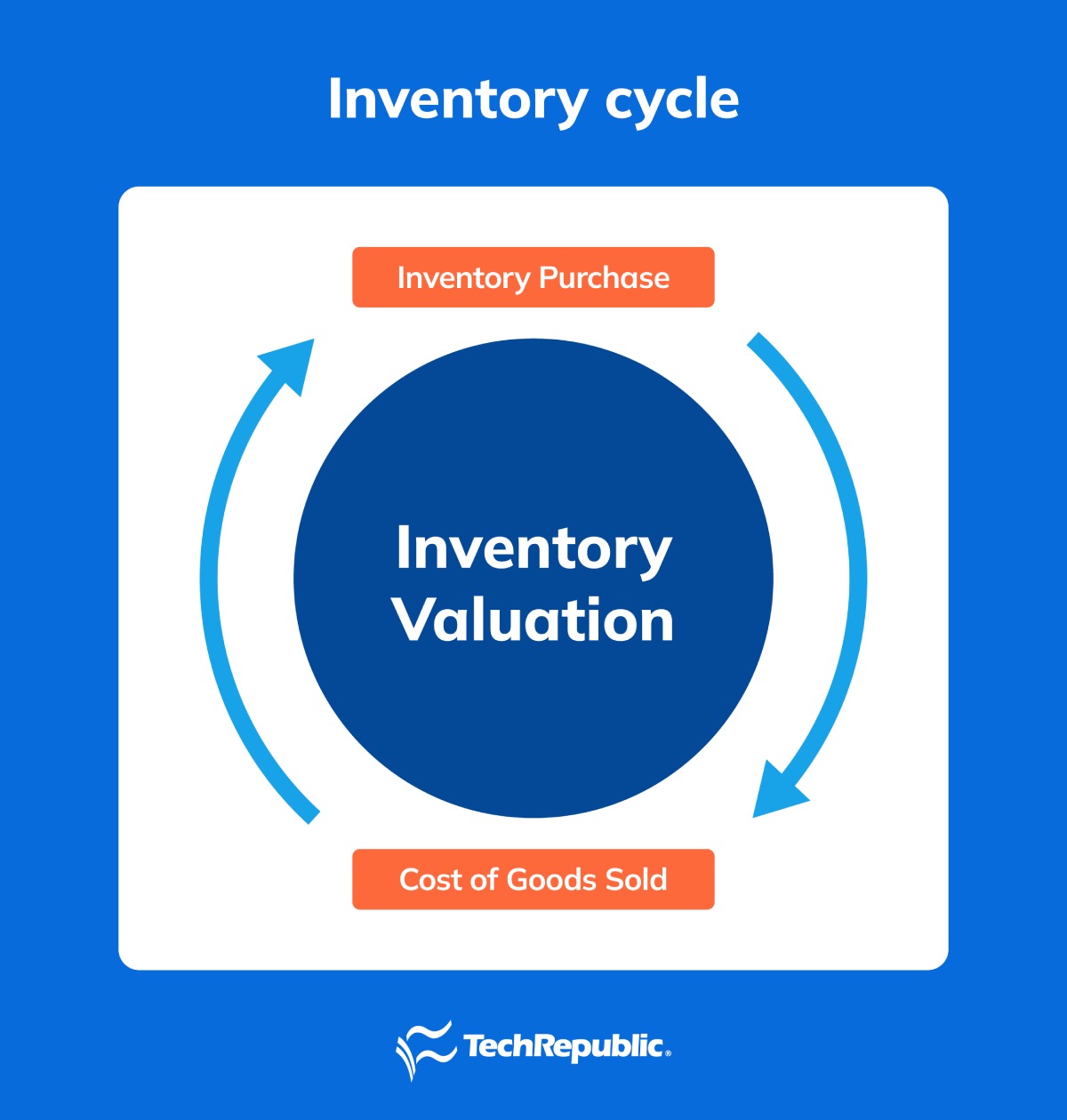

The inventory accounting cycle

Inventory accounting starts with the purchase of items intended for sale. The cycle of a single inventory item ends with the sale, when the cost of goods sold is recognized. But the entire sales cycle lives on, with more inventory being purchased and sold. Inventory valuation of unsold items is ongoing throughout the inventory accounting cycle. During this cycle, the following actions take place:

Inventory purchase: Items recorded as an asset

Inventory sale: COGS calculated

Inventory valuation: Performed periodically while the inventory items are held for sale

Inventory accounting methods

The most common inventory accounting methods are FIFO, LIFO, Weighted Average Cost, and Specific Identification. Each method affects cost of goods sold and ending inventory differently, which in turn impacts a company’s financial statements and tax liabilities.

| FIFO | Assumes oldest inventory sold first | During inflation, lower COGS than LIFO |

| LIFO | Assumes newest inventory sold first | During inflation, higher COGS |

| Weighted Average Cost | Averages cost of all units | Smooths out price fluctuations, reduces COGS volatility |

| Specific Identification | Tracks exact cost of specific items | reflects actual historical cost |

How inventory accounting affects financial statements

Inventory accounting impacts all three major financial statements. On the balance sheet, inventory is recorded as a current asset, directly affecting a company’s total asset value. On the income statement, the COGS reduces gross profit and ultimately net income. On the cash flow statement, inventory reduces cash flow when items are purchased and increases cash flow when items are sold, which comprehensively affects working capital.

Examples of inventory accounting methods

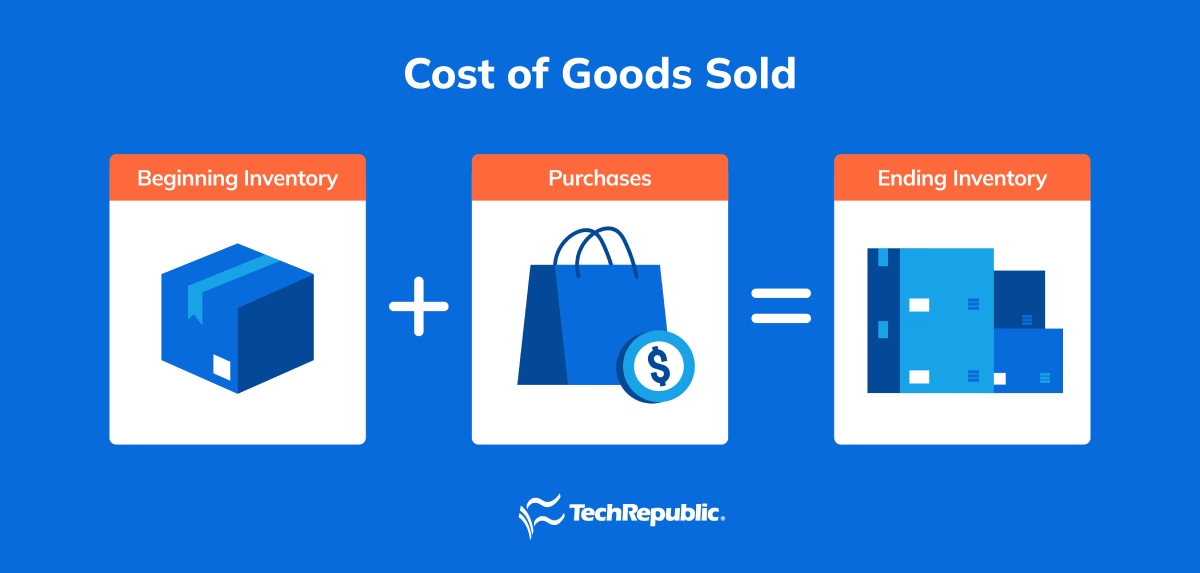

I’ll illustrate the impact of inventory accounting methods by using a sample shoe store to showcase the results in a case-specific fashion. For each method, we will use the basic formula for COGS. The examples below assume no beginning inventory.

Example of inventory accounting using FIFO

| Units purchased | Purchase price per unit | Total purchase price | |

| January | 100 | $40 | $4,000 |

| February | 100 | $50 | $5,000 |

| March | 100 | $60 | $6,000 |

| Total | 300 | $15,000 | |

Walk This Way Shoes sold 200 pairs of sneakers in March for $90 each, resulting in revenue of $18,000. With FIFO, the oldest inventory is sold first. This means that the first 100 pairs of shoes sold cost Walk This Way $4,000, and the second 100 pairs of shoes sold cost Walk This Way $5,000.

Beginning Inventory: 0

+ Purchases: $15,000

– Ending Inventory: $6,000

COGS: $9,000

By using this FIFO method of inventory management, the company sold the shoes that were purchased first and sitting on the shelf the longest, as opposed to selling the shoes most recently obtained in March. Walk This Way’s net profit was also $9,000 ($18,000 – $9,000 COGS). Let’s compare that net income to what would be received using the LIFO method.

Example of inventory accounting using LIFO

| Units purchased | Purchase price per unit | Total purchase price | |

| January | 100 | $40 | $4,000 |

| February | 100 | $50 | $5,000 |

| March | 100 | $60 | $6,000 |

| Total | 300 | $15,000 | |

Using the same fact pattern as before, Walk This Way Shoes sold 200 pairs of sneakers in March for $90 each, resulting in revenue of $18,000. With LIFO, the most recent inventory is sold first. This means that the first 100 pairs of shoes sold cost Walk This Way $6,000.

The second pair of 100 shoes sold cost Walk This Way $5,000. By using this LIFO method of inventory management, the company sold the shoes that were obtained most recently, as opposed to selling the shoes that were sitting on the shelf the longest.

Beginning Inventory: 0

+ Purchases: $15,000

– Ending Inventory: $4,000

COGS: $11,000

Walk This Way’s net profit was $7,000 ($18,000 – $11,000 COGS).

Example of inventory accounting using the Weighted Average method

| Units purchased | Purchase price per unit | Total purchase price | |

| January | 100 | $40 | $4,000 |

| February | 100 | $50 | $5,000 |

| March | 100 | $60 | $6,000 |

| Total | 300 | $15,000 | |

Using the same fact pattern as before, Walk This Way Shoes sold 200 pairs of sneakers in March for $90 each, resulting in revenue of $18,000.

Under the Weighted Average Cost per unit, the cost of shoes sold is calculated as follows:

Step one: Calculate the cost per pair. $15,000 total cost ÷ 300 pairs of shoes = cost of $50 per pair

Step two: Apply the cost per pair to the number of pairs sold. 200 pairs x $50 = $10,000

$18,000 gross revenue – $10,000 = $8,000 gross profit

Example of inventory accounting using the specific identification method

Let’s now imagine that Walk This Way specializes in the sale of autographed basketball shoes. Due to the unique nature of their product, they may only have a handful of inventory items on hand, and each item was purchased at a unique price.

| Units purchased | Purchase price per unit | Total purchase price | |

| January | 1 - signed by Michael Jordan | $4,000 | $4,000 |

| February | 1 - signed by Steph Curry | $5,000 | $5,000 |

| March | 1 - signed by Lebron James | $6,000 | $6,000 |

| Total | 3 | $15,000 | |

In March, Walk This Way sold the shoes autographed by Michael Jordan and Lebron James for $7,000 and $11,000 respectively for a total revenue of $18,000.

While timing is a key factor with the LIFO and FIFO methods, with the specific identification method, cost is assigned per unit, irrespective of when the item was purchased. Unlike the Weighted Average method, cost is not aligned with the cost of any other inventory items.

The cost for items under the specific identification method is $10,000 ($4,000 + $6,000).

Beginning Inventory: 0

+ Purchases: $15,000

– Ending Inventory: $5,000

COGS: $10,000

Under the specific identification method, Walk This Way’s net profit was $8,000 ($18,000 – $10,000 COGS)

More about Accounting

- What Is Accounting? Definition, Types, Importance and Examples

- Best Accounting Software and Services

- Verito vs. Rightworks: Which IT Provider Is Best for Your Firm?

- Top Free Accounting Software

- Accounting Glossary

Which inventory method is best?

For Walk This Way, the tax impact of inventory methods varied. Assuming a 25% tax rate, LIFO turned out to be the winner of the four inventory methods by generating the lowest tax bill of $1,750. By using LIFO, the business reported a lower profit of $7,000, but a tax savings of $500. This happened because newer, more expensive inventory was used in calculating COGS. This narrowed the gap between sales price and cost, which reduced profit but also reduced the related income tax.

- Income tax under FIFO method: 25% of $9,000 = $2,250

- Income tax under LIFO method: 25% of $7,000 = $1,750

- Income tax using the Weighted Average: 25% of $8,000 = $2,000

- Income tax using Specific Identification: 25% of $8,000 = $2,000

If Walk This Way’s objective is solely to reduce tax, LIFO might be the way to go. If they are more concerned with having a profit and loss statement that appeals to investors, FIFO might be preferred since it produces the highest net profit.

The best inventory method for each business depends on the factors at play in the economic environment. These factors include industry and product type, as well as price volatility. Businesses with perishable goods often use FIFO, while those managing rising costs may prefer LIFO. Tax implications, cash flow goals, and compliance requirements also play a role.

✅ Why use FIFO?

- Ensures older, often lower-cost inventory is used first, closely matching actual product flow.

- As prices increase over time, lower cost contributes to higher profits, which may appeal to investors or lenders.

- Inventory valuation is simple and transparent, making it easier for financial reporting and audits.

- Accepted under both GAAP and IFRS, making it ideal for international businesses.

✅ Why use LIFO?

- As prices increase over time, revenue may not be as high as other valuation methods, but taxable income will be lower; improving short-term cash flow in inflationary environments.

- Better reflects current market costs in the cost of goods sold

- Commonly used in industries with rapidly increasing inventory costs, like manufacturing, retail, or commodities.

- Permitted under US GAAP, though not allowed under IFRS — best for companies operating primarily in the US.

✅ Why use Weighted Average?

- Smooths out price fluctuations by averaging cost.

- Simpler tracking — no need to match specific batches or track oldest/latest inventory.

- Commonly used in businesses selling homogeneous items (like shoes, clothing, or groceries in bulk).

✅ Why use specific identification?

- Ideal when inventory items are unique or high-value, and cost tracking per unit is possible.

- Ensures precise matching of cost and revenue for each sale.

Best practices for inventory accounting

Managing inventory effectively is key to accurate financial reporting and operational efficiency. The following best practices can help ensure reliable inventory accounting:

- Choose the right valuation method (FIFO, LIFO, or Weighted Average) to align with your business goals and industry practices.

- Maintain accurate records by tracking inventory levels, purchases, sales, and adjustments — ideally in real time with a perpetual system. Try one of our best picks for the 5 Best Retail Accounting Software.

- Verify inventory regularly through physical or cycle counts, and separate employee duties to reduce errors and prevent theft.

Bottom line

Inventory accounting is a critical component of sound financial management and business strategy. The various methods of valuing and tracking inventory impact a company’s financial outcome. Ultimately, strong inventory accounting practices improve financial accuracy, aid compliance, support cash flow management, and enhance decision-making across business functions.

Frequently asked questions (FAQs)

What are the four types of inventory?

The four main types of inventory are raw materials, work-in-progress (WIP), finished goods, and maintenance, repair, and operations (MRO) supplies.

Is inventory accounting hard?

Inventory accounting can be complex, especially as businesses grow or deal with fluctuating costs and large product varieties, but with an understanding of basic methods, this important task is manageable.

Why is inventory accounting important?

Inventory accounting directly affects profitability and financial reporting. It also impacts business taxes and supports operational decisions.

What are the inventory accounting methods?

Common inventory accounting methods include FIFO, LIFO, Weighted Average Cost, and Specific Identification.

Can a business change its inventory accounting method?

Yes, but it must disclose the change and justify it under accounting standards.

How does inventory affect profitability?

COGS directly impacts gross profit; inaccurate valuation can distort profitability.

How often should inventory be counted?

Inventory should be counted at least annually. Businesses may also count their inventory on a more regular daily, weekly, or monthly cycle.