Neobanks are digital-first financial technology (fintech) companies that offer banking services entirely online, without needing physical branches. They leverage technology to provide core banking services through intuitive mobile apps and websites. As a banker, I see them as a modern alternative that is reshaping how businesses and individuals manage their money.

Key takeaways:

- Digital-first: Neobanks operate exclusively online, often through mobile apps.

- Partnerships: Many partner with traditional banks to ensure FDIC insurance and regulatory compliance.

- Cost-effective: They typically offer lower or no monthly fees due to reduced overhead.

- Feature-rich: Expect innovative tools like budgeting, expense tracking, and seamless software integrations.

- Convenience: Manage your finances anytime, anywhere, with quick account opening.

- Ideal for small businesses: Particularly suitable for small businesses, freelancers, and startups.

- What are neobanks?

- How do neobanks work

- Neobanks overall impact

- Pros and cons of neobanks

- Suitability for businesses

- How neobanks make money

- Buyer’s guide: Choosing a neobank

- Featured neobanks for businesses

- Relay Relay is a fintech and not a bank. Deposits qualify for up to $3,000,000 in FDIC insurance coverage when placed at program banks in the Thread Bank deposit sweep program. Deposits at each program bank become eligible for FDIC insurance up to $250,000, inclusive of any other deposits you may already hold at the bank in the same ownership capacity.

- Bluevine Bluevine is a financial technology company, not a bank. Deposits are FDIC insured up to $3,000,000 per depositor through Coastal Community Bank, Member FDIC and other program banks.

- North One North One is a financial technology company, not a bank. All banking services are provided by The Bancorp Bank N.A., Member FDIC.

- Novo Novo is a fintech, not a bank. Banking services provided by Middlesex Federal Savings, F.A. Member FDIC.

- Frequently asked questions (FAQs)

What are neobanks?

As a banker, I define neobanks as agile financial institutions that exist entirely online. Unlike traditional banks with physical branches, neobanks operate only through apps and websites. That’s why they are often called challenger banks or digital banks, because they challenge the old branch-based model.

What sets them apart is their focus on convenience, transparency, and modern technology. By keeping everything digital, they can streamline services, cut down on fees, and offer a smoother customer experience compared to the more complex, branch-dependent world of traditional banking.

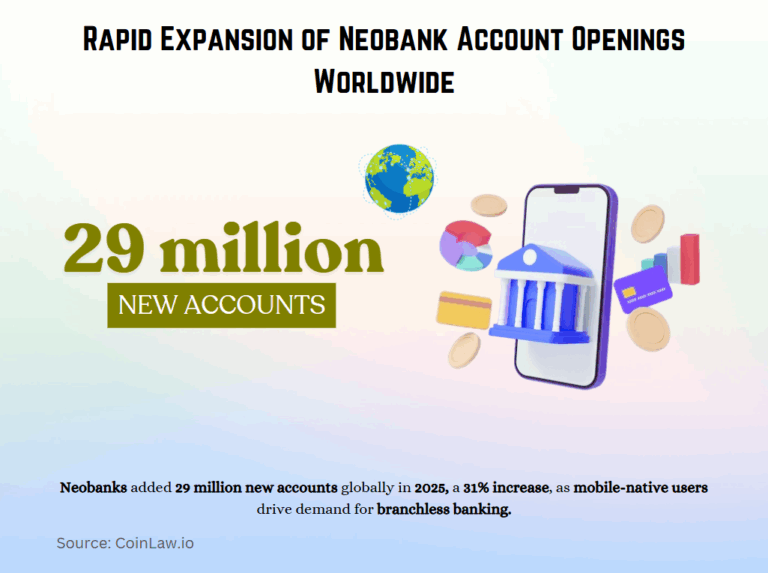

According to Coinlaw.io, a surge of 29 million new neobank accounts in 2025 highlights just how quickly digital-only banking is becoming mainstream. The 31% jump reflects how mobile-native customers are increasing demand for branchless, technology-first solutions. Instead of relying on physical locations, business owners and consumers alike are rapidly adopting the speed and convenience of digital technology.

How do neobanks work

You might be wondering, how do neobanks work without physical branches? The answer is simple. They run entirely online through websites and mobile apps. Because they don’t have the costs of maintaining buildings or staff in branches, they can pass those savings on to customers with little to no fees.

Many neobanks partner with traditional banks to handle the background work. This setup gives them access to the same secure systems that big banks use and makes sure customer deposits are protected, often through FDIC insurance in the U.S. Put simply, your money is kept safe like it would be at a regular bank, but you also get the modern features and convenience that come with fintech banking.

To make things even smoother, neobanks rely on automation, artificial intelligence for customer service, and cloud technology. This lets them offer faster support, simple tools for managing money, and a user-friendly experience that fits right into daily life.

Everyday examples of how this looks for customers

- Opening an account takes just a few minutes from your phone.

- You receive instant alerts every time you use your debit card.

- You can send money to a friend without logging into a separate payment app.

- Chat with AI-powered support any time of day instead of waiting on hold.

- Use built-in budgeting tools that track spending automatically.

Neobanks overall impact

Neobanks are shaking up modern finance, and the key to how neobanks work lies in their digital-first design. Their growth has prompted traditional banks to enhance their digital presence and improve customer service. For you, that means more options, easier tools, and better service.

They’re also helping more people get access to basic banking. Communities that were once left out of the system, or people who never had a bank account before, can now open accounts and use tools to manage their money. On top of that, neobanks are especially appealing to younger generations like Gen Z and Millennials, who want simple apps, lower fees, and a smooth digital experience that fits their lifestyle.

What this looks like in real life

| Early access to paychecks | Get your paycheck up to two days before payday. |

| Round-up savings | Spare change from purchases is automatically saved into a savings account. |

| International convenience | Use your card abroad without huge foreign transaction fees. |

| Smarter alerts | Get instant notifications if unusual spending is detected. |

| Card control | Freeze or unfreeze your debit card from the app in seconds. |

Pros and cons of neobanks

Like any financial choice, neobanks come with both advantages and trade-offs. For many people, the benefits of low fees, quick account setup, and modern tools make them an attractive alternative to traditional banks.

At the same time, their digital-only model isn’t the right fit for everyone, especially those who prefer in-person service or need a broader range of financial products. A good example is a customer who needs daily access to physical cash exchange services.

| Pros | Cons |

|---|---|

|

|

Suitability for businesses

As a banker, I can confidently say that neobanks are increasingly suitable for businesses, especially small businesses, startups, and freelancers. Their digital-first nature and cost-effectiveness make them a compelling choice.

They cater to businesses that value efficiency and prefer to manage their finances entirely online, often providing some of the best online business accounts for managing money with lower fees, easier access, and modern tools.

- Cost-effectiveness and transparency: Businesses can benefit from reduced or no monthly fees, competitive foreign exchange rates, and lower transaction charges due to neobanks’ lower operating costs. Many also offer transparent pricing, making it easier to understand your banking expenses.

- Convenience and efficiency: Mobile-first interfaces and online account management allow business owners to conduct banking anytime, anywhere. They offer quick account setup and faster transaction processing, freeing up valuable time.

- Automation and integration: Many neobanks provide automated financial tools and seamlessly integrate with popular accounting software like QuickBooks and Xero. This saves time on administrative tasks and reduces manual errors, streamlining your financial operations.

- Scalability and niche focus: Some neobanking solutions offer scalable services and tiered plans that can adapt as your business grows. Many specialize in particular financial products or customer groups, tailoring services to unique business needs.

- Global accessibility: For businesses involved in international transactions or looking to expand globally, neobanks can offer competitive foreign currency exchange and international money transfers, often at better rates than traditional banks. However, it’s crucial to assess your specific needs, as some neobanks may not support certain traditional business services like physical check payments or extensive cash handling.

How neobanks make money

Neobanks employ various strategies to generate revenue, especially given their lower operational costs compared to traditional banks. Their business model is lean, relying on digital efficiency.

A significant portion of their revenue comes from interchange fees, which are small amounts paid by merchants each time a customer uses their debit or prepaid card. Many also offer subscription fees or premium accounts, providing additional features like enhanced customer support, higher transaction limits, or advanced financial tools for a monthly fee.

Some neobanks offer loans, credit cards, or overdraft protection, earning revenue from the loan interest charged on these products. While often offering low or no fees for accounts, some may charge small transaction fees for specific services like out-of-network ATM withdrawals, cross-border payments, or foreign exchange.

Finally, partnerships and referral programs with third-party financial service providers (e.g., insurance, investment platforms) can generate commissions. Some even monetize their technology infrastructure by providing API access or white-label solutions to other companies, earning revenue through licensing.

Buyer’s guide: Choosing a neobank

When considering a neobank for your business, it’s essential to evaluate your specific needs and priorities. Think of this as your personalized buyer’s guide for digital banking.

| Category | What to look for |

|---|---|

| Fees and rates | Transparent pricing, low or no fees for services like transfers, ATM withdrawals, and cash deposits; competitive interest rates on savings/checking. |

| Account types & features | Options for business checking and savings, multiple sub-accounts; tools like budgeting, early direct deposit, virtual cards, payroll, and accounting software integration. |

| FDIC Insurance | Verify deposits are FDIC-insured (usually via partner bank) up to $250,000 per depositor, per account type, per bank. |

| Customer support | 24/7 access by phone, chat, or AI-driven assistance, since there are no branches. |

| Security features | Strong protections like encryption, multi-factor authentication, biometrics, real-time alerts, and card freezing. |

| Integration capabilities | Seamless connections with QuickBooks, Xero, Stripe, PayPal, and other essential business tools. |

| Scalability & coverage | Ability to grow with your business; support for multiple currencies and international transactions. |

| Cash handling | Options for deposits/withdrawals if your business deals with cash; be aware that many neobanks have limits or fees here. |

These considerations will help you choose a neobank that best fits your business model and operational preferences.

Featured neobanks for businesses

As an experienced banker, I’ve seen many new players emerge. Here’s a look at some leading neobanks that are making waves for business owners:

Relay

Relay is a popular neobank focusing on comprehensive cash flow management and team collaboration. It’s particularly appealing for small to medium-sized businesses and solopreneurs seeking robust digital banking.

| Feature area | Details and comparisons |

|---|---|

| Accounts |

|

| Features |

|

| Fees |

|

Bluevine

Bluevine is a popular neobank that primarily offers business checking accounts. It’s known for competitive interest rates and a transparent fee structure.

| Feature area | Details and comparisons |

|---|---|

| Accounts |

|

| Features |

|

| Fees |

|

North One

NorthOne offers specialized business accounts with a strong emphasis on integration and financial tracking.

| Feature area | Details and comparisons |

|---|---|

| Accounts |

|

| Features |

|

| Fees |

|

Novo

Novo’s model simplifies things with integrated tools and typically no fees, primarily appealing to online small businesses and freelancers.

| Feature area | Details and comparisons |

|---|---|

| Accounts |

|

| Features |

|

| Fees |

|

Frequently asked questions (FAQs)

What is the primary difference between a neobank and a traditional bank?

Neobanks operate entirely online, without physical branches, primarily through mobile apps and websites. Traditional banks, in contrast, offer services both in person at branches and online.

Are deposits in neobanks safe and insured?

Yes. Neobanks partner with traditional banks to ensure FDIC coverage up to $250,000 per depositor, per account type, per bank.

Can I deposit cash with a neobank?

Some neobanks offer options for cash deposits, typically through partnerships with retail networks like Green Dot or ATM networks like Allpoint+. However, these often come with fees and daily/monthly limits. Some do not support direct cash deposits at all, so it’s important to check at account opening.

Are neobanks suitable for small businesses and freelancers?

Absolutely. Neobanks are increasingly popular for small businesses, startups, and freelancers due to their lower fees, digital-first convenience, and integrations with accounting software. They streamline financial management for modern business needs.

What are the main drawbacks of using a neobank?

The primary drawbacks include the lack of physical branches for in-person service or complex cash transactions, and potentially a more limited range of financial products (e.g., mortgages, extensive loan options) compared to traditional banks. Reliance on technology means service can be affected by outages.