I evaluated the following buy now, pay later companies based on transaction fees, revenue impact, supported regions and industries, and integration options to help determine which best suits your business needs:

- Best for integrations and high-ticket sales: Affirm

- Best for PayPal merchants: PayPal Pay Later

- Best for native marketing tools: Klarna

- Best for businesses that use Square: Afterpay

- Best for customized payment terms: Zip

- Best for e-commerce: Shop Pay Installments

Buy now, pay later apps allow customers to split their purchases into multiple installments, often interest-free, while merchants receive full payment upfront. This financing model increases average order value (AOV), enhances conversion rates, and attracts a wider customer base. Below is an overview of the best BNPL companies, comparing key considerations to give a better idea of what each provider offers for different business types.

Top buy now, pay later companies compared

| Merchant processing fees | Sales channel integrations | Integration types | Supported locations | |

|---|---|---|---|---|

| Affirm | Typically 5.99% + $0.30 | In-store, mobile (in-app), ecommerce, online marketplace, telesales | Plug-and-play, APIs | U.S., U.K., Canada |

| PayPal Pay Later | 4.99% + $0.49 | Mobile (in-app), ecommerce | Automatic, custom APIs | All PayPal locations |

| Klarna | 5.99% + $0.30 | In-store, mobile (in-app) | APIs, Plug-and-play for UK businesses | North America, Europe, U.K. |

| Afterpay | Custom | In-store, mobile (in-app), ecommerce | Plug-and-play, APIs | U.S., U.K., Australia, New Zealand |

| Zip | Custom | In-store, mobile (in-app), ecommerce | Plug-and-play, APIs | U.S., Australia, New Zealand |

| Shop Pay Installments | Typically 5.99% + $0.30 | In-store, ecommerce | Plug-and-play | U.S. |

SEE: Why BNPL Skyrocketed During the 2024 Holiday Season

Affirm: Best for integrations and high-ticket sales

Affirm specializes in financing high-value purchases with extended repayment terms, making it ideal for businesses selling expensive products. It offers multiple integration options and supports any business with a U.S., Canadian, or UK bank account. Affirm lets customers pay in four interest-free payments every two weeks and/or installments for up to 36 months.

Why I chose Affirm

Affirm sets itself apart with its high spending limit and long financing terms, making it a better choice for businesses selling luxury or high-ticket items than Klarna, which has a broader but more general financing structure. I also like how it supports multiple integration options, so businesses can use Affirm for in-person, online, marketplaces, mobile, and even telesales.

Pricing

- Merchant fees: Based on business type and services but typically 5.99% + $0.30 per transaction

- Customer fees: 0% APR for pay-in-four; monthly financing APR from 10% to 36%

Visit Affirm

Features

- From $50 to $30,000, providing flexibility for high-ticket items

- Payment options of 4 installments or monthly plans of up to 36 months

- Compatible with Shopify, BigCommerce, and WooCommerce, allowing seamless integration for online stores

How to integrate Affirm with your business platform: Affirm supports five different integration types designed for various payment methods, including in-person and e-commerce. Visit Affirm’s integration documentation.

Pros & Cons

| Pros | Cons |

|---|---|

| Wide range of compatible platforms | Requires a minimum AOV of $50 |

| No late fees for customers | Interest rates as high as 36% for extended loans |

| Transparent pricing | Funding takes up to 3 business days |

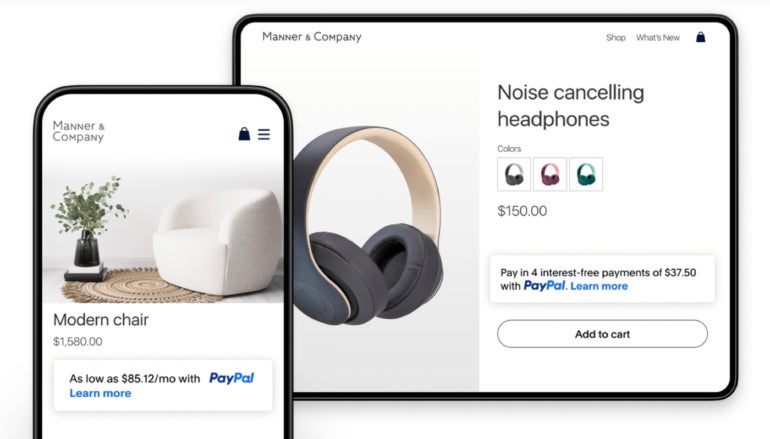

PayPal Pay Later: Best for PayPal merchants

PayPal Pay Later is the native buy now, pay later solution from PayPal. The solution is pre-integrated into PayPal Business accounts, providing seamless checkout for businesses already using PayPal as a payment processor. PayPal offers the traditional BNPL zero interest with Pay in 4, while PayPal Credit is for extended monthly payment options.

Why I chose PayPal Pay Later

As the pioneer in digital payment solutions, PayPal’s seamless integration is unmatched, making it the go-to BNPL solution for businesses already using PayPal. Merchants have the advantage of attracting over 400 million people using the platform. However, unlike competitors such as Afterpay and Klarna, PayPal lacks in-store compatibility.

Pricing

- Merchant fees: 4.99% + $0.49 per transaction

- Customer fees: 0% APR for Pay in 4; monthly financing APR from 9.99% to 35.99%

Visit PayPal

Features

- Pay in 4 (bi-weekly up to 6 weeks) and pay monthly (3, 6, 12, or 24 months) options

- Financing for $30-$1500 (Pay in 4) or $49-$10,000 (pay monthly)

- Automatic integration for all PayPal merchants

- Pay Later messaging to promote Pay Later offers on your e-commerce website

How to integrate PayPal Pay Later with your business platform: In addition to the standard BNPL integration, advanced customizations are available via PayPal Checkout APIs. Visit PayPal’s API documentation.

Pros & Cons

| Pros | Cons |

|---|---|

| No additional setup for PayPal merchants | Not available for in-store purchases |

| Lower processing fees compared to competitors | Higher late fees than some competitors |

| PayPal purchase protection |

Klarna: Best for native marketing tools

Klarna offers a comprehensive BNPL solution with multiple financing options for customers and robust merchant support, including marketplace exposure and seamless e-commerce integration. Its diverse financing options and strong brand presence make it an ideal choice for businesses looking to cater to a broad customer base.

Why I chose Klarna

Unlike PayPal Pay Later, which is limited to PayPal transactions, Klarna integrates with multiple platforms, providing a more extensive reach. I also like Klarna’s growing partnerships with merchant acquirers and payment processors, such as Adyen and Stripe. But what makes Klarna stand out is its suite of native marketing tools, including in-app ads, personalized content, and store locator maps.

Pricing

- Merchant fees: 5.99% + $0.30 per transaction (US & Canada)

- Customer fees: 0% APR for Pay in 4 & Pay in 30; monthly financing APR from 7.99% to 33.99%

Visit Klarna

Features

- Pay in 4, Pay in 30, or monthly installment financing (up to 36 months) payment plans

- Financing $35 to $1,000 (Pay in 4, Pay in 30) or above $1,000

- Supports major e-commerce platforms and payment processors

- Klarna app and physical card for in-store purchases

How to integrate Klarna with your business platform: Klarna provides API integration tools for U.S. merchants. Visit Klarna’s integration documentation.

Pros & Cons

| Pros | Cons |

|---|---|

| Multiple financing options | Plug-and-play integration only for UK merchants |

| No preset loan limits | 12-month merchant contract required |

| Low APR for extended loans | Late fees for customers ($7 to 25% of loan value) |

Afterpay: Best for businesses that use Square

Afterpay specializes in interest-free pay-in-four installments and is popular among retailers that cater to Gen Z and millennial shoppers. It was acquired by Square’s parent company, Block, and now offers a simple plug-and-play integration to its point of sale (POS) software. Afterpay also offers API-based integration for popular e-commerce platforms, including Shopify.

Why I chose Afterpay

Most reviews praise Afterpay for its focus on young shoppers. But it’s Afterpay’s seamless Square integration that clearly sets it apart from other providers in this guide. With Square’s feature-rich free all-in-one POS plan, even merchants with a very limited budget can stay competitive. The provider also integrates with popular e-commerce and payment processors but not as extensively as Klarna.

Pricing

- Merchant fees: Custom fees based on business profile and services required or 6% + $0.30 (with Square)

- Customer fees: No interest on pay-in-four; late fees range from $8 to 25% of the purchase value

Visit Afterpay

Features

- Pay in 4 and pay monthly terms of up to 12 months.

- Financing starts with up to $100 (Pay in 4) and increases based on the customer’s payment history, or $200 to $5,000 (Pay monthly)

- In-depth shopper insights from the merchant dashboard.

- Offers both online and mobile-first approach with in-app payment solutions

How to integrate Afterpay with your business platform: Supports both plug-and–play as well as RESTful APIs for custom integration. Visit Afterpay integration documentation.

Pros & Cons

| Pros | Cons |

|---|---|

| High customer adoption among Gen Z and millennials | Funding takes up to 5 business days |

| Seamless integration with Square POS | Late fee for missed payments |

| Stripe, Adyen, and other payment processor integration | Merchants in certain U.S. states are not eligible for Pay Monthly financing* |

| *Nevada, West Virginia, Hawaii, New Mexico | |

SEE: POS Terminals Explained By Experts: A Complete Guide

Zip: Best for customized payment terms

Zip (formerly Quadpay) is a buy now, pay later solution that offers various financing options based on the user’s credit standing. It supports both online and in-app payments, as well as in-person transactions at the point of sale via a physical and virtual (contactless) card. Like its more popular counterparts, Zip partners with big brands such as Amazon, Walmart, Target, and Nike.

Why I chose Zip

Zip stands out among other BNPL providers in this list for allowing shoppers to adjust the payment terms on outstanding BNPL loans (refinancing). While it may cost customers more, letting shoppers know that they have this option gives Zip a unique marketing advantage. I’m also impressed with Zip’s high user ratings on both iOS and Android apps, though, like Affirm, its serviced regions are very limited.

Pricing

- Merchant fees: Custom fees based on Zip’s assessment of your business profile

- Customer fees: 0% APR for pay-in-four; interest applies for extended financing. Pay date change fee: $2

Visit Zip

Features

- Pay in 4 and Pay in 8 options

- Financing limit depends on Zip’s assessment of creditworthiness.

- Customizable payment terms for outstanding loans

- No code, low code, and API integration options for online and in-store transactions

How to integrate Zip with your business platform: Zip supports custom API and Javascript SDK for merchant-initiated gateway API integration. Visit Zip API documentation.

Pros & Cons

| Pros | Cons |

|---|---|

| Highest iOS and Android app user reviews among providers on this list | Higher fees for customers who opt for extended financing |

| Allows customers to split payments interest-free | Limited international availability |

| Strong e-commerce and POS integration |

Shop Pay Installments: Best for e-commerce

Shop Pay Installments is Shopify’s branded buy now, pay later solution embedded into its one-click checkout button Shop Pay. The app is powered by Affirm but is customized to work with Shopify’s advanced omnichannel and multichannel features, including detailed sales tax management, lead generation, marketing, and order and fulfillment tools. While Shopify can integrate with other BNPL providers, a native solution is a more cost-efficient option for merchants.

Why I chose Shop Pay Installments

I gave Shop Pay Installments its place in this guide because, in addition to potential conversion rate boosts from Shop Pay one-click checkout, Shopify’s e-commerce capabilities are simply unmatched. And with its own installment solution pre-integrated into every Shopify e-commerce merchant account, businesses can offer Affirm’s high credit limits and several term options with just a simple integration.

Pricing

- Merchant fees: Based on business type and services but typically 5.99% + $0.30 per transaction

- Customer fees: 0% APR for pay-in-four; monthly financing APR from 10% to 36%

Note: Shopify charges businesses a monthly fee for using its platform on top of merchant fees.

Visit Shop Pay

Features

- Installment options for transactions between $35-$30,000

- Payment options of 4 installments or monthly plans of up to 36 months

- BNPL built into Shopify’s one-click checkout feature

- One integration setup for both online and in-person transactions

How to integrate Shop Pay Installments with your business platform: Developer tools available for customizing checkout forms. Visit Shop Pay Installments documentation.

Pros & Cons

| Pros | Cons |

|---|---|

| Advanced e-commerce management tools | Limited to U.S. merchants |

| One-click checkout | Requires Shopify Payments and Shop Pay |

| 24/7 customer support |

SEE: The 4 Best E-commerce Payment Solutions

What's hot at TechRepublic

- Blackpoint Cyber vs. Arctic Wolf: Which MDR Solution is Right for You?

- Why AWS Sellers Choose Deepgram Over Other Voice AI Tools

- SS&C Intralinks DealCentre AI vs. Datasite: Which platform is built for the future of dealmaking?

- SS&C Intralinks FundCentre AI vs. Juniper Square: Which platform better supports modern private markets fund managers?

- Verito vs. Rightworks: Which IT Provider Is Best for Your Firm?

How to integrate BNPL into your checkout

Here is a six-step guide for integrating BNPL into your checkout process:

Step 1: Evaluate your current checkout process. Identify potential bottlenecks like slow page loads, complex forms, and limited payment methods.

Step 2: Configure API or Plugin integration.

- For API-based BNPL providers: Work with developers to implement the provider’s API into your checkout.

- For plug-and-play integrations: Install the BNPL plugin through your e-commerce platform’s marketplace.

Step 3: Implement the integration. Ensure proper handling of customer authentication and eligibility checks, payment installment calculations, and error handling and transaction validation.

Step 4: Test for functionality and UX. Conduct test transactions, monitor for errors, and gather user feedback.

Step 5: Ensure compliance and security. Encrypt transactions, implement fraud detection, and comply with PCI DSS and GDPR.

Step 6: Optimize for mobile and UX. Simplify checkout, ensure mobile responsiveness, and personalize the payment journey. Also, enhance the customer experience by:

- Displaying BNPL prominently: Showcase BNPL options on product pages, checkout screens, and marketing banners.

- Providing clear installment breakdowns: Help customers understand repayment terms.

- Ensuring mobile-friendly design: Adapt BNPL UI elements to enable seamless mobile transactions.

SEE: Best Mobile Credit Card Processing Solutions

Choosing the right BNPL provider for your business

To select the best BNPL solution, businesses should consider:

- Transaction costs: The fees charged to merchants for processing BNPL transactions, including percentage-based fees and fixed costs per transaction

- Financing flexibility: The ability to offer short-term, interest-free installment plans or longer-term financing with potential interest rates

- Integration requirements: Seamless integration with major e-commerce platforms and POS systems, ensuring a smooth checkout experience for both merchants and customers

- Location and industry compatibility: The extent to which the BNPL provider operates in your desired locations and industry, ensuring customer service availability

- Scalability: The platform’s ability to adapt to and continue to integrate with your business system upgrades and requirements

- Security measures: The provider’s ability to match your business system’s security protocols for protecting customer data, such as PCI compliance and machine learning fraud detection tools

- Customer demographics: Understanding whether your target audience comprises younger, budget-conscious Gen Z shoppers or high-ticket buyers looking for long-term financing options

By carefully evaluating these factors, businesses can implement a BNPL solution that enhances customer experience, increases sales, and aligns with their financial strategy.